BUSINESS PERFORMANCE

OUR PERFORMANCE

The year 2011 was filled with accomplishments and challenges. The environment of economic growth in Brazil, in spite of the crisis in developed countries, continued to propel the insurance market, which saw a nearly 16% growth over 2010. The insurance industry penetration in Brazil represents development opportunities, chiefly due to the expansion of the emerging Brazilian middle class.

Within this context, 2011 continued to single us out in terms of quality of service, service delivery, and convenient solutions for more than six million families and corporate clients.

We work with three auto insurance brands: Porto Seguro, Itaú Auto, and Azul Seguros. With these, we meet the various needs of our different audiences, our insurance brokers, and our policyholders.

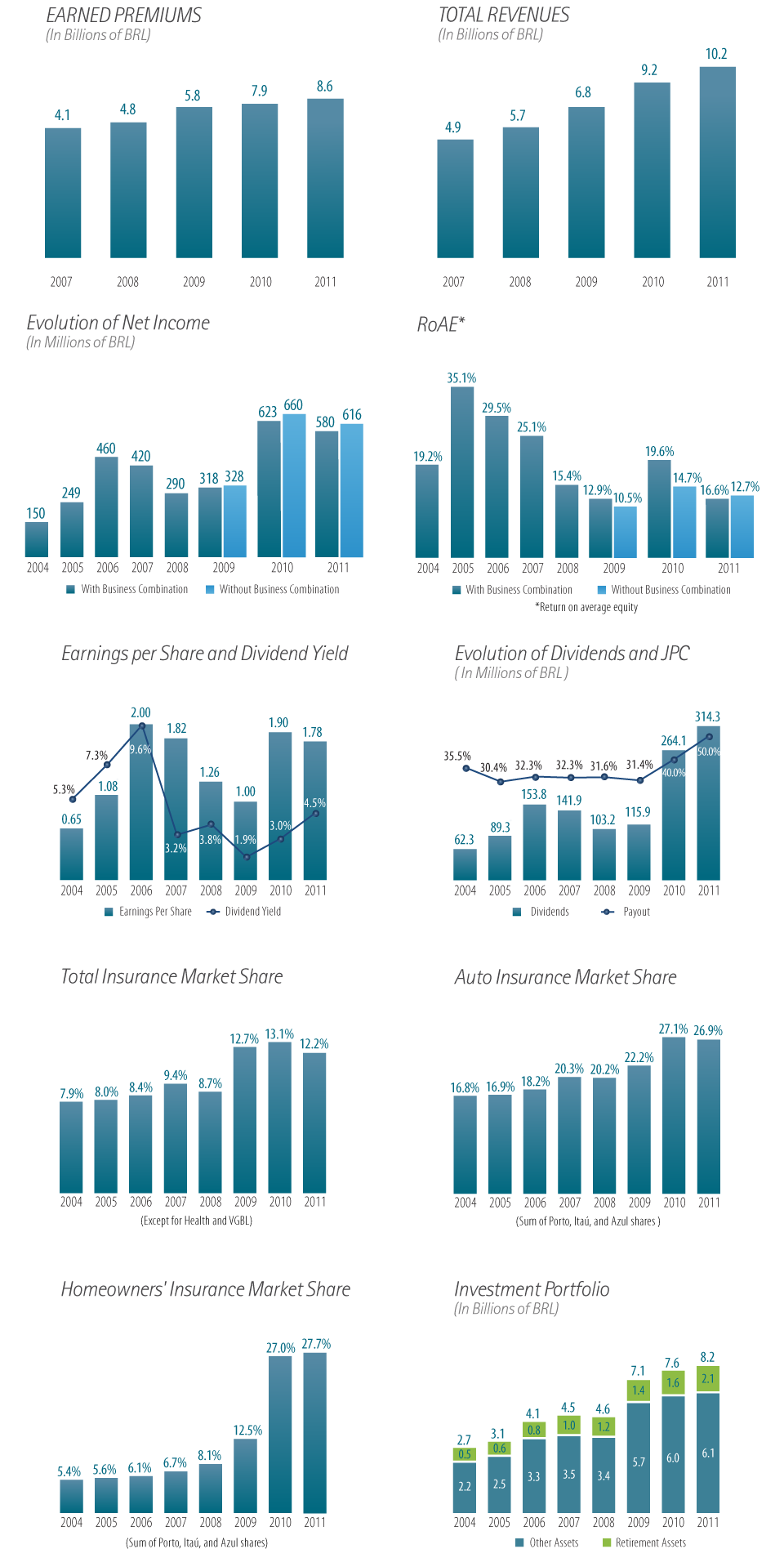

We ended 2011 with nearly 4.1 million insured vehicles and a total of over 11.6 million items covered by our products, which represents a 32% increase over the previous year. Earned premiums amounted to BRL 8,426 million, with a BRL 661 million or 8.5% increase over the sum of BRL 7,765 million in 2010, which does not factor in the Brazil-specific Roth individual retirement accounts (VGBL, acronym in Portuguese).

In addition, we took on the challenge of managing Itaú Seguros' tow truck and guaranteed hire car services. Now, three companies are managed by only one platform. The integration of auto insurance assistance resulted in a 28% growth in the volume of tow truck and guaranteed hire car services that are managed by Porto Socorro.

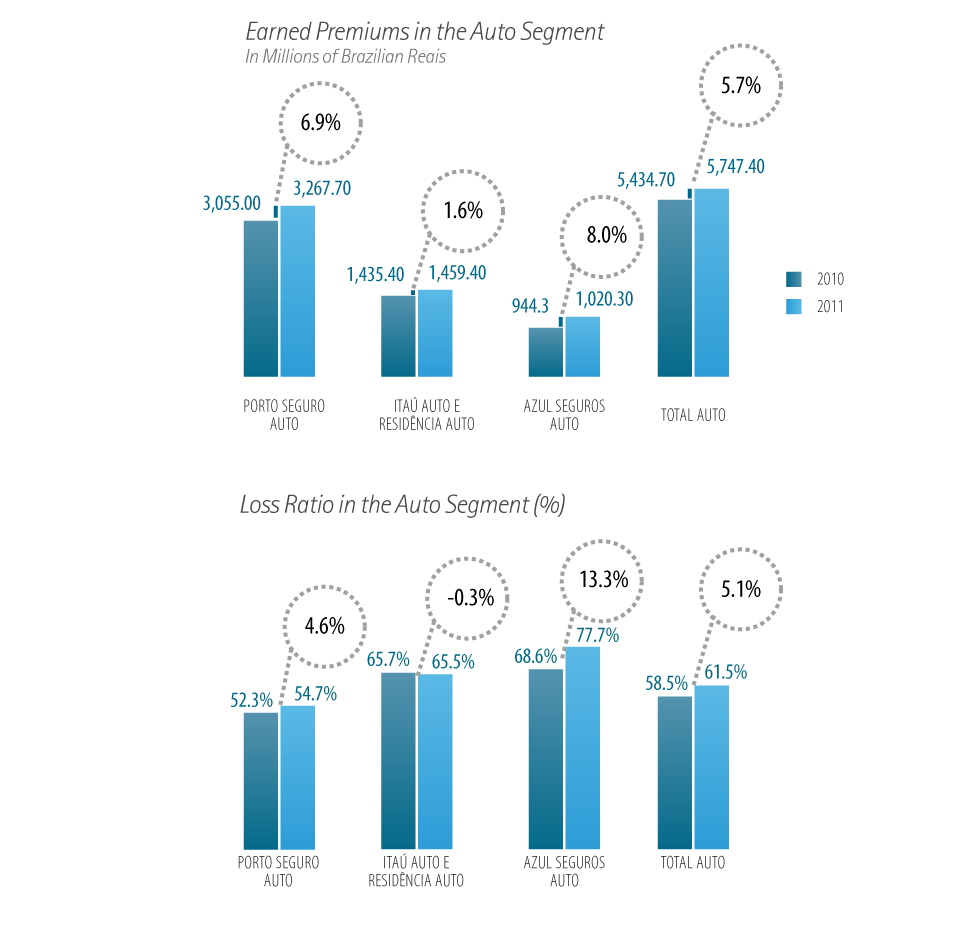

Our results also singled us out in terms of growth of total revenue, which, including net finance revenue, added up to BRL 10,155 million, a growth of BRL 979 million or 10.7% over the BRL 9.176 million during the previous year. In 2011, earned premiums amounted to BRL 5,747 million, an increase of BRL 312 million or 5.8% over the sum of BRL 5,434 million in 2010.

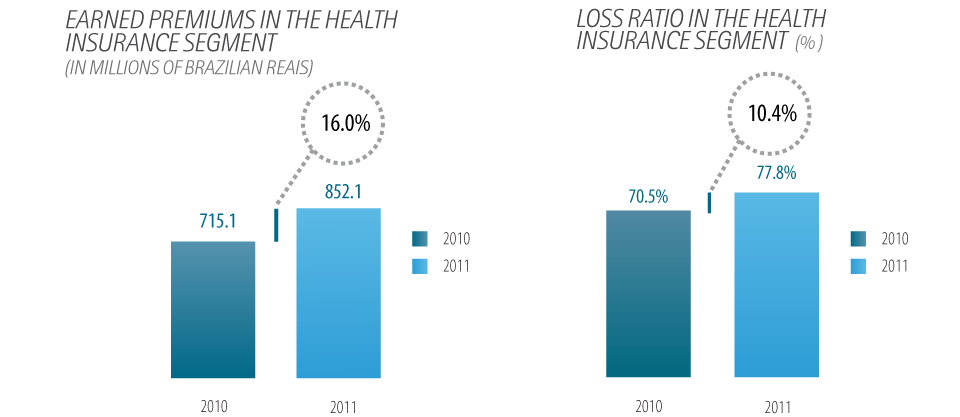

In turn, earned premiums for the health insurance segment worked out at BRL 852 million in 2011, with a BRL 137 million or 19.2% increase over the sum of BRL 715 million in 2010. In 2011, our policyholders and their dependents amounted to 567,000, a 27% increase over the 447,000 figure in 2010. In 2011, our net income added up to BRL 580 million, recording a 6.9% decrease over the BRL 623 million we earned in 2010. This decrease is mainly due to an increase in retained loss expenses and the necessary administrative costs to sustain our outstanding service strategy.

The year 2011 was also filled with investments. We repositioned the Itaú Auto e Residência brand, which now relies on special benefits for Banco Itaú account holders. We continued to invest in the improvement of our research park and our operational and business relations with insurance brokers. Additionally, we enhanced both results and operational structure of other businesses, such as credit card, financing, consórcio, monitored alarms, among others. Income from such businesses grew by about 27% over 2010.

I would also like to emphasize that we established Porto Seguro Telecomunicações S.A., a company that provides phone services. We optimized the internal management of cell phone costs. In addition, we seized the opportunity of bringing together our insurance products to add mobility to our clients and insurance brokers.

Within the context of campaigns and actions, I would like to emphasize the Porto Vias campaign, a service that provides drivers with real-time traffic information over notebooks, smartphone applications, or desktop computers.

The driver, either in São Paulo or Rio de Janeiro, chooses the best way to get to his or her destination. I would also like to emphasize the Trânsito+Gentil movement, a Porto Seguro Auto initiative for drivers to avoid aggressive behavior and treasure a more tolerant attitude while driving as well as a quality-of-life program for employees, training for service providers, and policyholder benefits, such as cultural and food discounts.

I would like to thank all of our employees, providers, and insurance brokers, who did their job with dedication and commitment, during 2011.

In 2011, we continued to excel in quality of service, service delivery, and convenient solutions for more than six million families and corporate clients.

Porto Seguro Auto: premiums amounted to BRL 3,267,7 million, a 6.9% increase over 2010. This performance stemmed from a 10.9% growth in the insured fleet, which worked out at 2,088,600 in 2011, a factor that was partially balanced by a 3.5% decrease in the average annual premium due to a change to the client mix. Our loss ratio grew 2.4% as a result, chiefly because of an increase in the frequency of theft and larceny, mostly in São Paulo State.

Itaú Auto e Residência: premiums amounted to BRL 1,459,4 million, a 1.6% increase over 2010. There was a 0.4% decrease in the insured fleet, which amounted to 1,064,000 vehicles at the end of the year. Loss ratio fell by 0.2% over the previous year. This performance, which was relatively stable when compared to 2010, stemmed from brand repositioning, system integration, and adjustments to the risk selection criteria and other operational adjustments.

Azul Seguros: premiums amounted to BRL 1,020,3 million, an 8% increase over 2010. This performance stemmed from a 16.7% growth in the insured fleet, which worked out at 960,500 in 2011, a factor that was partially balanced by a 7.4% decrease in the average annual premium. Our loss ratio experienced a 9.1% decrease, mostly because of a stronger competitive environment.

With an increase of BRL 137 million (16.0%) over the BRL 715.1 million in 2010, earned premiums for this segment worked out at BRL 852.1 million in 2011. This comes as a result of a 567,400 (27%) increase in policyholders and dependents in 2011 over the 446,800 figure in 2010. Our loss ratio amounted to 77.8%, a 7.3% increase over the previous year, due to an increase in the medical inflation rate, the utilization frequency, and changes to policy adjustments, which became annual, in compliance with the ANS Rule No. 1950.

Annuities: premiums amounted to 351.5 million, a 9.8% increase over 2010. This growth stemmed chiefly from an increase in the number of policyholders and their dependents. Our loss ratio amounted to 30.3%, an improvement arising chiefly from the cancellation of loss-making policies for the period.

Retirement: income from retirement plan deposits worked out at BRL 293.2 million in 2011, an increase of BRL 40.6 million (16.1%) over the BRL 252.6 million figure for 2010. This performance stemmed from a 7.2% increase in the number of plan holders, which were 149,000 in 2011, and in average deposits.

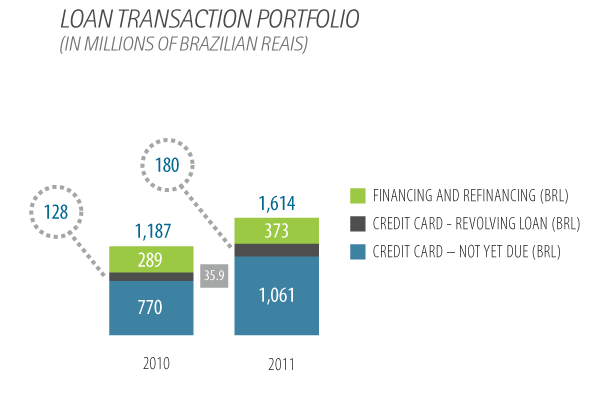

Income from loan transactions worked out at BRL 211.2 million in 2011, an increase of BRL 42.5 million (25.2%) over the BRL 168.7 million figure for 2010.

This performance stems chiefly from a 38.2% increase in credit card transactions. The portfolio with managed credit transactions grew by 35.9% and went to BRL 1,616.3 million (including the sum of installments to mature) from the BRL 1,187.0 million in 2010.

Monitoring: income from the delivery of electronic-monitoring services amounted to BRL 66.2 million in 2011, an increase of BRL 8.5 million (14.7%) over the BRL 57.7 million figure for 2010. The number of clients experienced a 14.6% increase and jumped to 28,300. In 2010, clients amounted to 24,700. Our annual income average for service delivery was 10.5% lower in 2011 and worked out at BRL 2,343,700 over the BRL 2,617,200 figure for 2010.

Consórcio: income from consórcio management amounted to BRL 156.5 million in 2011, an increase of BRL 22.8 million (17.0%) over the BRL 133.7 million figure for 2010. The number of consórcio units that we managed experienced a 41.9% increase and jumped to 89,100 in 2011 over the 62,600 figure for 2010.

Other Income from Services: Income from other services rendered pertain chiefly to Crediporto, Porto Seguro Serviços, Porto Seguro Atendimento, Portopar (Asset Management) and investment property revenues. In 2011, it worked out at BRL 131 million, an increase of BRL 42.9 million (48.7%) over the BRL 88.1 million figure for 2010. This performance stemmed from an increase in income from all our main services companies. Porto Seguro Serviços (220.1%) and Porto Seguro Atendimento (77.5%) were the year's highlights.